Although it is up 43% YTD, Snap, Inc (NYSE: SNAP) is witnessing some concerning signs due to the slowdown in active users growth as well as the decline in average revenue per user. Based on these factors it is highly likely that the company misses on its revenue estimates in its Q2 earnings set to be released on July 25 after hours. Despite this, the company has been adding subscribers to its Snap+ service and could be on track for an EPS beat in its Q2 earnings. In light of this, SNAP stock could be one to watch closely ahead of its earnings.

SNAP Stock News

Decelerating Growth

SNAP’s position as a social media company means that user growth is its most important metric, since no matter how good the product, is no one is going to use a platform that no one else uses. This makes the decelerating user growth the company is seeing a major concern as its daily active users’ growth has been decelerating for 2 straight quarters now.

The decelerating growth can be attributed to the stagnation the North American market is seeing. SNAP has maintained 100 million DAU in North America for three quarters straight.

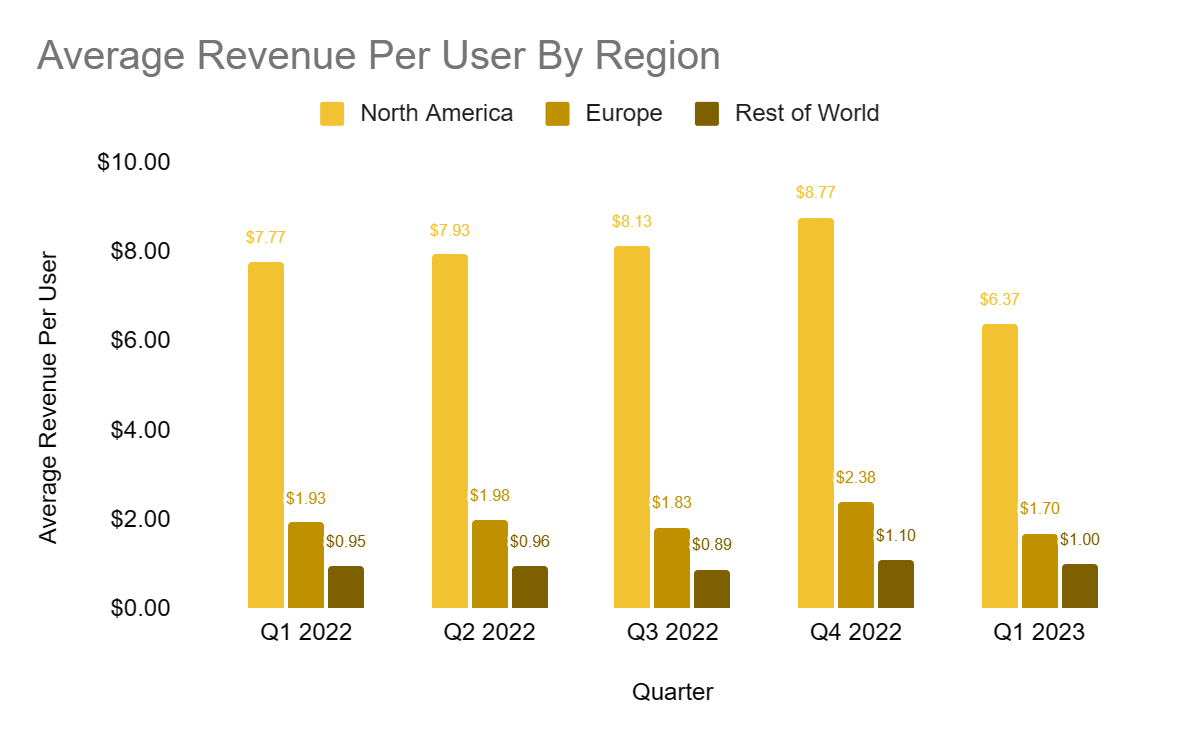

What makes this worse for SNAP is that North America has the highest average revenue per user (ARPU) amongst all regions, and countries outside of North America and Europe which are seeing the highest growth in DAU have the lowest ARPU.

Another thing to take into consideration is while North America has by far the highest ARPU compared to other regions, North America is currently seeing the lowest ARPU since Q2 2021. While it is concerning, it also means that SNAP still has room to improve its revenues if it can return to the previous levels of ARPU in North America.

Snap+ and My AI

While SNAP has suffered from slower growth in almost every area of its business, its subscription service Snap+ has grown more than 33% QoQ from 3 million subscribers to 4 million subscribers. With the subscription costing $3.99, that means that SNAP will realize around $48 million in quarterly revenue and $192 million annually from Snap+ alone. Furthermore, Evan Spiegel, SNAP’s CEO, said that more than 150 million users have used the new chatbot My AI since it was released to all of its users. While My AI can’t compete with other Large Language Models (LLMs) like Microsoft’s (NASDAQ: MSFT) ChatGPT, it can be another way that SNAP can increase its ad revenue since it can use sponsored links that are relevant to the conversation which it has already tested in May.

Q2 Forecast

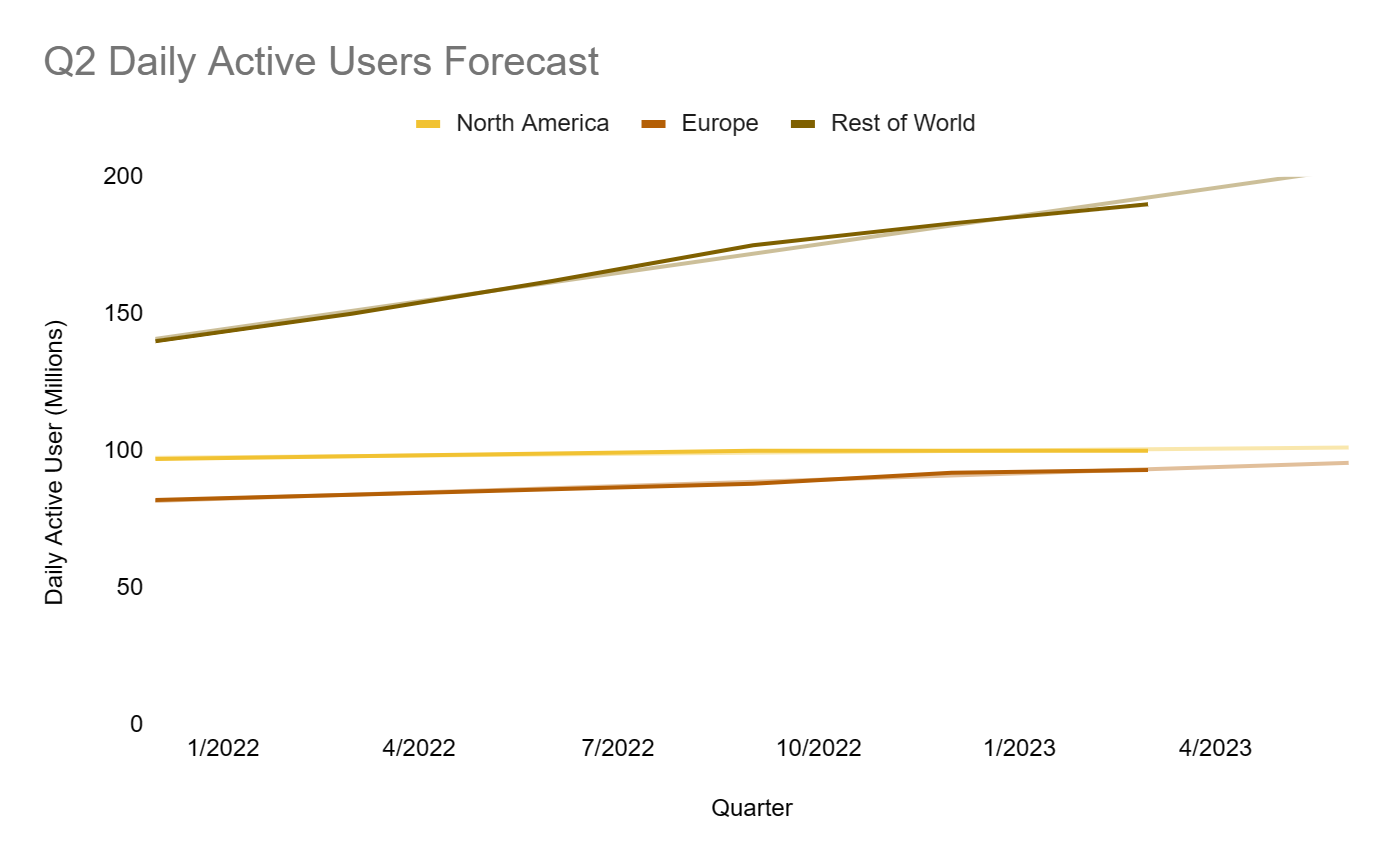

Using SNAP’s DAU numbers for the last 6 quarters, its estimates for North America, Europe, and RoW are around 101.2 million, 95.6 million, and 202.89 million respectively. According to the linear regression trendlines in the chart below, total DAUs can be forecasted to be around 399 million users.

That would mean that SNAP’s revenues would reach $1.01 billion assuming the ARPU it recorded in Q1 2023 stays roughly the same. Adding revenue from the new one million subscribers to SNAP+ would make SNAP’s total Q2 revenues around $1.022 billion which is less than analyst estimates of $1.054 billion.

Furthermore, SNAP’s cost of revenue and operating expenses are expected to remain relatively flat according to management at around $440 million and $910 million, respectively. This means that SNAP would record a net loss of $328 million and an EPS of -$0.205, which is better than analysts’ estimates of -$0.247. For this reason, SNAP stock could be set to run on an EPS beat – especially with the stock trading near the lower trendline of its upward channel.

| (All in millions except EPS) | |

| Revenue | $1,022.00 |

| DAU | 399 |

| ARPU | $2.56 |

| Cost of Revenue | $440.00 |

| Operating Expenses | $910.00 |

| Net Loss | $328.00 |

| EPS | -$0.21 |

SNAP Stock Financials

In its Q1 2023 report, SNAP’s total assets decreased 1.25% QoQ from $8 billion to $7.9 billion due to a decline in its accounts receivable. While its cash and cash equivalents increased 13% QoQ from $1.4 billion to $1.58 billion due to $100 million of free cash flow being generated in Q1 2023. SNAP’s total liabilities decreased by 2% QoQ from $5.4 billion to $5.3 billion.

Revenue also decreased 7% YoY from $1.06 billion to $0.988 billion due to the decline in ARPU. Operating costs stayed roughly the same compared to last year at around $914 million. While operating loss decreased 8.5% YoY from $351 million to $321 million due to an increase in interest income from investments in government securities. This all amounted to a net loss of $328 million – a 9% decrease YoY.

Media Sentiment

@thisisorlando is bullish on SNAP’s options flow ahead of its Q2 earnings.

@AllllSevens believes SNAP stock could surpass the $30 mark by the beginning of 2024.

Technical Analysis

SNAP stock’s trend is bullish with the stock trading in an upwards channel. Looking at the indicators, the stock is trading below the 50, and 21 MAs which is a bearish indication, and above the 200 MA which is a bullish indication. Meanwhile, the RSI is neutral at 40 and the MACD is approaching a bullish crossover.

As for the fundamentals, the upcoming Q2 2023 earnings will be a catalyst for SNAP stock. If SNAP beats its EPS estimates it can cause its stock to maintain its momentum and run which makes the current PPS an attractive entry point ahead of earnings as the stock is currently testing the lower trendline.

SNAP Stock Forecast

While SNAP is working on increasing its ad revenue using its My AI chatbot and its Snap+ subscription, it is currently seeing stagnation in its active users’ growth in North America – its biggest market revenue-wise. That said, there is a strong possibility SNAP stock runs post earnings as it may beat EPS estimates based on our calculations. With the stock trading at the lower trendline, bullish investors could find a good entry into SNAP stock at current levels in anticipation of its Q2 earnings on July 25 after hours.

If you have questions about SNAP stock and where it could be heading next feel free to reach out to us in our free alerts room!

Disclaimer

Please visit and read our disclaimer here.