Affirm Holdings, Inc. (NASDAQ: AFRM) is a BNPL service provider that rose to prominence during the pandemic. Currently, the stock is up more than 60% since releasing its 2023 annual report, despite the Fed’s tightening policy showing its impact on the company’s operations. With the student loan repayments resuming last month after a 3-year pause, the company may struggle in the coming quarters as consumers will have to choose between paying rent, buying food, and paying their BNPL loans. Meanwhile, its cost of capital is high due to the high interest rates which may impact its bottom line. Considering the underwhelming earnings and guidance by fellow fintech startup Upstart Holdings, Inc. (NASDAQ: UPST), AFRM stock may be poised to lose all the gains it made in recent months on its guidance when it reports on November 8th after hours.

AFRM Stock News

Fed’s Policy is Squeezing Consumers

The high interest rate environment has severely impacted customer spending. In the Commerce Department’s final revision of Q2 GDP, consumer spending was revised to a .8% annualized rate, significantly down from the 1.7% reflected in the previous estimate. All in all, spending in Q2 grew at its slowest pace since Q1 2022 when it was flat.

Despite this, BNPL use is still growing with 46% of Americans saying they’ve used such loans which is up from 43% last year, according to a survey conducted by LendingTree (NASDAQ: TREE). Since Affirm is one of the leading BNPL providers, it wasn’t surprising to see the lender grow its customers by 18% YoY in Q4 2023 to 16.5 million. That said, this increase may not be positive as more consumers are using BNPL services to make ends meet.

The aforementioned survey found that 27% of BNPL users use these loans as a bridge to their next paycheck amid rampant inflation, high interest rates, and growing layoffs. In addition, these loans are being used to purchase groceries with 21% of BNPL users having used at least one of such loans to buy groceries.

At the same time, the survey found that 40% of users have paid late on at least one of their loans. That being said, it’s worth noting that BNPL users have a lower credit rating than non-BNPL borrowers.

In a Consumer Financial Protection Bureau (CFPB) survey, BNPL borrowers had an average credit score in the range of 580 – 669 which makes them “subprime borrowers”. Meanwhile, consumers who don’t use BNPL have an average score in the range of 670 – 739 which is the prime range.

Furthermore, about half of BNPL users had less cash and savings than what they paid for their BNPL purchases. This means that these users wouldn’t be able to afford those purchases without borrowing which could be due to them having a credit card utilization rate between 40% and 50%.

Another finding of the survey was that BNPL users were 11% more likely to have a delinquency of at least 30 days. The difference between BNPL users and non-BNPL users is especially clear when looking at their store and credit card debts. 9% of BNPL users with credit cards missed payments of 30 days or more, compared to only 3% of non-BNPL borrowers. Additionally, 8% of BNPL users were late making payments on their store cards, compared to 1% of consumers who don’t use BNPL.

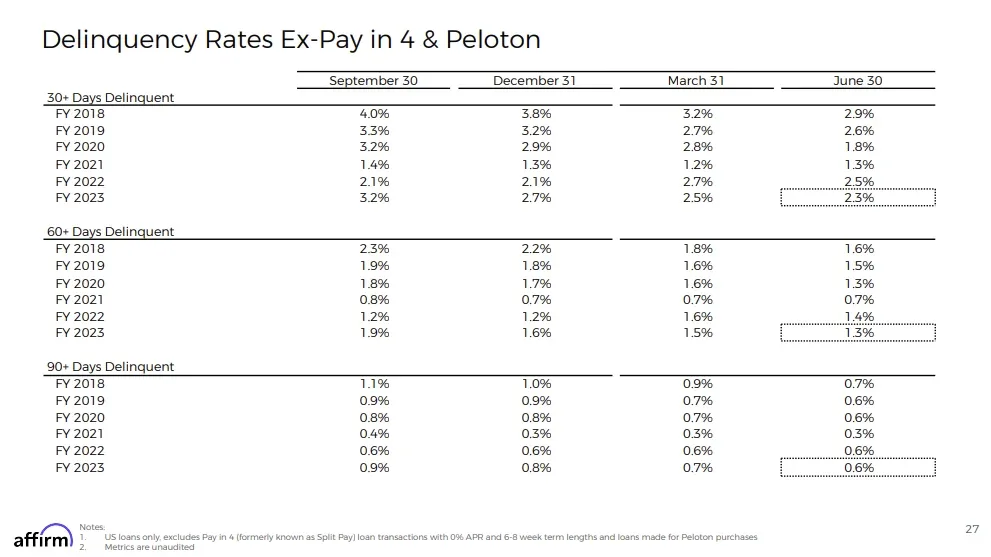

While Affirm’s delinquency rates remained near last year’s levels, they could start increasing in the next 2 quarters given that the company’s fiscal year ends on June 30. This means that its last reported figures don’t take into consideration the hardships faced by consumers.

Therefore, the company’s Q1 and Q2 2024 earnings reports will be critical to get a better picture of how the current macro environment will impact both its top line and bottom line, especially with the resumption of student loan repayments.

Student Loan Repayments Will Deal Another Blow

With student loan repayments resuming this month, this will certainly add more pressure on consumers. Goldman Sachs analysts expect the resumption of student loan payments to cost households around $70 billion per year which would subtract .8% from consumer spending in Q4 2023, slowing it down to 1.4%, per their estimates.

As a result, Affirm’s gross merchandise value (GMV), which is the total value of transactions, could witness decelerating growth or even decline in the coming quarters. The company’s GMV already witnessed decelerating growth in Q4 2023 as it grew 25% YoY compared to 76% in Q4 2022 due to the current macro environment.

This is further proof that consumers are spending more cautiously, and with student loan repayments resuming, consumers’ excess savings are likely to further shrink, tightening their credit. As a result, AFRM may report another decelerating GMV growth in its upcoming Q1 earnings.

Tightening Policy is Showing Its Impact

In addition to student loan payments, the current high interest rates could further impact Affirm’s earnings in the coming quarters after the Fed’s tightening policy started to show its impact on the company’s operations in Q4 2023. Since Affirm is not a bank, it doesn’t have customer deposits that it can use to fund its BNPL loans. Therefore, it partners with banks or issues bonds to raise the capital required to lend its customers. As interest rates are at a 22-year high, Affirm’s cost of capital is increasing which makes it more expensive for it to make BNPL loans.

This was evident in the company’s Q4 2023 earnings with its revenue less transaction costs declining 1% YoY as the benefits of larger volume could not outweigh inflated financing obligations. RLTC is a critical metric for BNPL providers since it measures the profitability of the business by subtracting the funding costs from the revenue generated from BNPL transactions. Moreover, the higher interest rates have led Affirm’s funding costs in FY 2023 to increase by a staggering 163% YoY. As such, it is clear that interest rates are starting to impact the profitability of the company’s business.

That said, the company has implemented a number of pricing initiatives to offset the impact of the high interest rates. These initiatives include increasing its maximum APR from 30% to 36%, offering low APR loans ranging from 4% to 9.99% as an alternative to monthly 0% APR programs, as well as shortening loan lengths and minimum order sizes for monthly 0% APR programs.

However, these initiatives may cause the company’s customers to use other BNPL providers that offer better terms when making their purchases, especially with the resumption of student loan repayments that will add pressure on consumers as discussed earlier.

Looking ahead, most analysts anticipate the Fed will hike rates one more time in 2023 to ultimately achieve a restrictive policy stance sufficient to curb inflation. Further tightening would serve to increase Affirm’s cost of borrowing and squeeze loan margins. In this way, there is little room for the company to compensate through volume alone without more aggressive repricing that endangers its customer base.

Upside Risks

The main risk to AFRM stock’s bearish thesis is if consumer spending doesn’t get impacted by the resumption of student loans. Mizuho analysts estimate the resumption of student loan repayments to present a 2% headwind to the BNPL industry’s growth volume which is insignificant. Also, Mizuho found in a survey that consumers with student loan debt tend to have higher incomes compared to those who don’t. As such, Affirm may not be impacted by this event, however, it is worth noting that BNPL users who have student loan debt use more BNPL services than those who aren’t repaying student loans which could prove to be an issue for the company’s business.

Media Sentiment

@TicTocTick expects AFRM stock to crash in a similar fashion to UPST stock.

@CorneliaLake is bearish on AFRM’s business model.

Technical Analysis

On the hourly chart, AFRM stock is in a neutral trend, however, it recently broke its sideways channel between $16.4 and $21.3. Looking at the indicators, the stock is above the 200, 50, and 21 MAs which is a bullish sign. Meanwhile, the RSI is neutral at 63 and the MACD is bearish.

As for the fundamentals, AFRM’s upcoming Q1 earnings on November 8th after hours will be a major catalyst, especially after UPST’s results. Considering the tough macro environment for BNPL providers, the company may report underwhelming financials and guidance which could see the stock fall near the $16 support. Therefore, investors could start a short position in the stock in the $22 to $20 range.

AFRM Stock Forecast

While more Americans are using BNPL services this year compared to last year, they are facing trouble paying off their loans. With student loan repayments resuming last month, consumers will be under more pressure as they will have to choose between paying rent, buying groceries, repaying their student loan debt, and paying BNPL loans. This could have catastrophic impacts on Affirm as its delinquency rates may increase in FY 2024.

At the same time, the resumption of student loan repayments is expected to slow down consumer spending amid the high interest rates. On that note, the current macro environment reflected on Affirm’s Q4 earnings as its GMV growth decelerated from 76% last year to 25% which means that consumers are already spending more cautiously without accounting for student loan repayments. Meanwhile, the company’s RLTC declined 1% YoY, indicating that the profitability of its business is under threat since this means that its cost of capital is high. Given that these headwinds may severely impact Affirm’s top line and bottom line in FY 2024, investors may find it lucrative to take a short position in its stock.

If you have questions about AFRM Stock and where it could be heading next feel free to reach out to us in our free alerts room!

Disclaimer

Please visit and read our disclaimer here.